The latest total value sales data from UK Builders’ Merchants show a continuation of the strong growth seen throughout 2021, as Q3 recorded the second-highest quarterly BMBI sales ever, just 2.4% behind Q2’s record breaking figures. However, there are signs of a slowdown as volume growth gives way to value growth, driven by price increases.

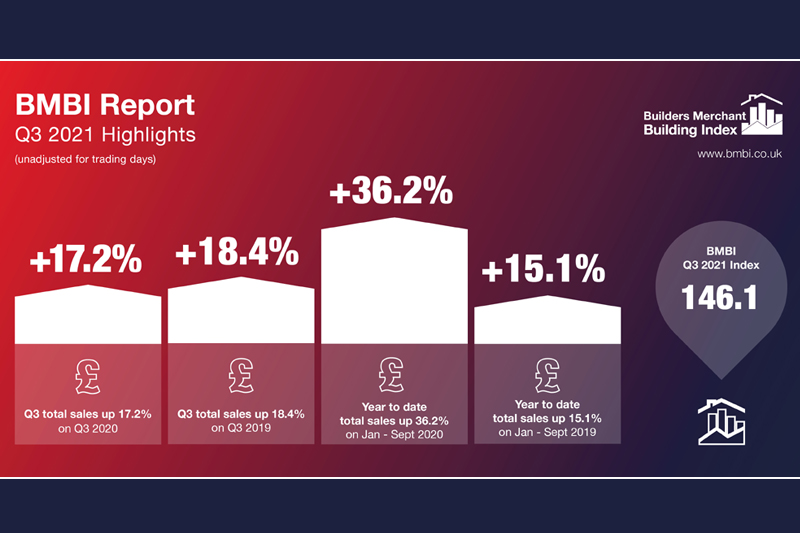

Total value sales in Q3 2021 were 17.2% higher than Q3 2020, with one less trading day this year. Eleven out of the 12 product categories sold more over the period. Timber & Joinery Products led the field (+43.9%) with its highest-ever quarterly BMBI sales, contributing significantly to overall growth. Excluding Timber, total merchant sales still grew by 9.6%. Like-for-like-sales increased by 19.1%.

Comparing Q3 2021 with Q3 2019, a more normal pre-Covid year, overall value sales were up 18.4% with one less trading day this year. Six categories sold more, led by Timber & Joinery Products (+48.9%) and Landscaping (+30.2%). Like-for-like sales were up 20.2%.

Quarter-on-quarter, sales were down 2.4% in Q3 compared to Q2, despite the three extra trading days in Q3. Five of the 12 product categories sold more in Q3 with Kitchens & Bathrooms (+7.4%) and Timber & Joinery (+4.8%) performing best. Of the seven categories that sold less in Q3 than Q2, the largest category, Heavy Building Materials was -2.1% down while seasonal category Landscaping was weakest (-22.5%). Like-for-like sales were 7.0% lower than in Q2.

Month on month

A robust September performance contributed to Q3’s performance, with total merchant sales 6.2% higher than August, with one more trading day. All bar one category sold more.

Compared to September 2020, total sales were up 14.9% in September 2021. Timber & Joinery Products (+38.7%) did best and continues to outperform other categories. However, Kitchens & Bathrooms (+11.8%) also recorded its highest-ever BMBI monthly sales.

Total value sales in September 2021 were 24.5% higher than the same month two years ago, with one more trading day this year. Much of this growth is owed to Timber & Joinery Products (+54.1%) and Landscaping (+40.2%). Without these two categories in the calculations, the two-year growth is still strong at +13.3%.

The Q3 BMBI index was 146.1, with nine of the 12 product categories exceeding 100. Timber & Joinery (191.9) and Landscaping (184.0) continue to outperform other categories by some margin. However, Heavy Building Materials (133.3), Ironmongery (126.2) and Kitchens & Bathrooms (125.3) also did well. Renewables was the weakest category (71.2).

Year to date performance

Year-to-date the sector is up by 36.2% in value, with this noticeably ahead of some of the growth forecasts made at the beginning of the year.

Commenting on the latest BMBI report, BMF CEO John Newcomb said: “Despite the issues in supply and pricing merchants have experienced throughout 2021, they are continuing to manage these challenges and deliver product to customer sites. While there are some signs that demand is starting to ease, Blocks, Lintels, Sheet Materials and Timber have again had record quarters, with Bricks and Insulation not far behind Q2’s record figures.”

Emile van der Ryst, Senior Client Insight Manager – Trade at GfK added: “The final quarter of the year should see further sales easing, but still moving along very well. Supply chain issues are reducing, but wider UK market sentiment suggests this could persist until 2023. Pricing will most likely continue to drive any value growth.

“It’s safe to say that the final year figures will be noticeably ahead of initial forecasts, but we expect that 2022 will see a decline against this most exceptional year.”

Mike Rigby, CEO of MRA Research, commented: “This year has been just as unexpected as 2020 for merchants, but for more positive reasons, with the most recent quarter showing a continuation of the strong growth experienced throughout 2021. Year-to-date, the sector is up by 36.2% in value over 2020, and 15.1% ahead of the same period in 2019!

“That’s way ahead of growth forecasts made at the beginning of the year. However, the sector is now starting to see the first signs of easing as price increases take over from volume sales to drive value growth. Housebuilding and infrastructure projects continue to boost sales, with heavyside activity – such as the astounding growth of timber and landscaping sales and the strong performance of heavy building materials – driving growth.

“The final quarter of the year is likely to see a slowdown in demand, as merchants’ sales return to more manageable levels after an exceptionally busy year. Supply chain problems seem to be easing, but a consensus in the market suggests these could persist until 2023 so we are not out of the woods. But it’s safe to say, that end of year figures will be noticeably ahead of initial forecasts in an exceptional year.”

Developed and run by MRA Research, the BMBI – a brand of the Builders Merchant Federation – is a monthly index of builders’ merchant sales, and the most reliable, up-to-date measure of Repair, Maintenance, and Improvement (RMI) activity in the UK. The index is based on actual sales from GfK’s Builders’ Merchant Point of Sale Tracking Data, which captures value sales out to builders from generalist builders’ merchants, accounting for over 80% of total sales from builders’ merchants throughout Great Britain.

An in-depth review, which includes commentary by sector experts, is provided each quarter.

To download the Q3 2021 BMBI report, visit www.bmbi.co.uk.