The latest survey responses suggest that merchants’ expectations and confidence eased in September.

While the market is still buoyant, with a V-shaped recovery, merchants are cautious about the next three to six months. The ongoing threat from the pandemic and its impact on the economy and employment is weighing on merchants’ minds.

The Pulse, by MRA Research, is a monthly tracking survey of merchants’ confidence and prospects. Telephone interviewing took place between 1-8 September.

Impact of COVID-19

All branches we interviewed in September were open, and nearly two thirds are open fully. While new restrictions announced by the Government during September do not have a direct impact on branch opening times, more announcements and restrictions are expected to control the virus as we head into the winter months — and these may have a wider impact on businesses by the time this survey is published.

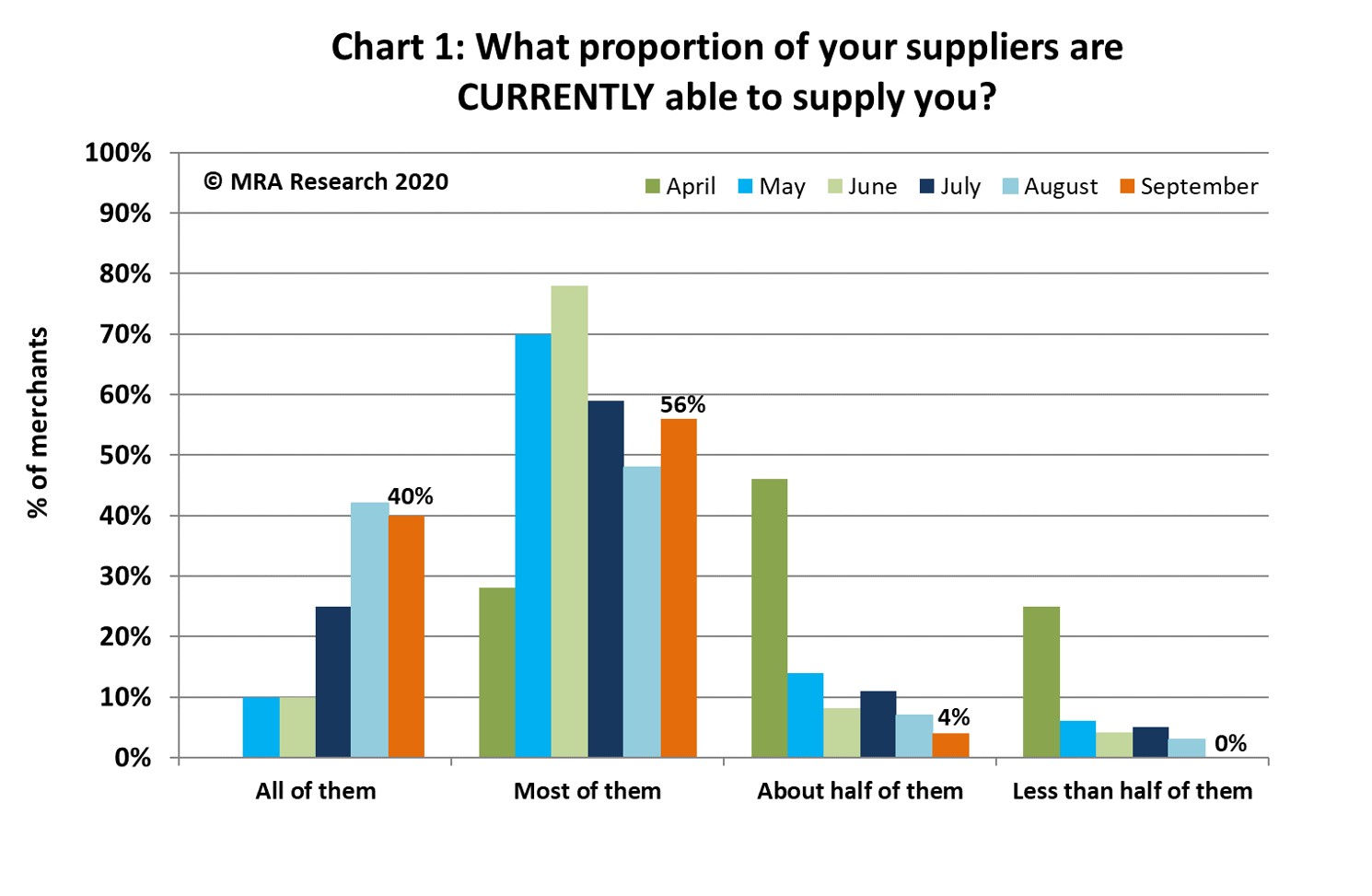

Material supply continued to improve in September, with over 90% of merchants reporting that all or most of their suppliers are now able to supply them — see Chart 1. However, longer lead times and stock shortages remain an issue.

Sales expectations

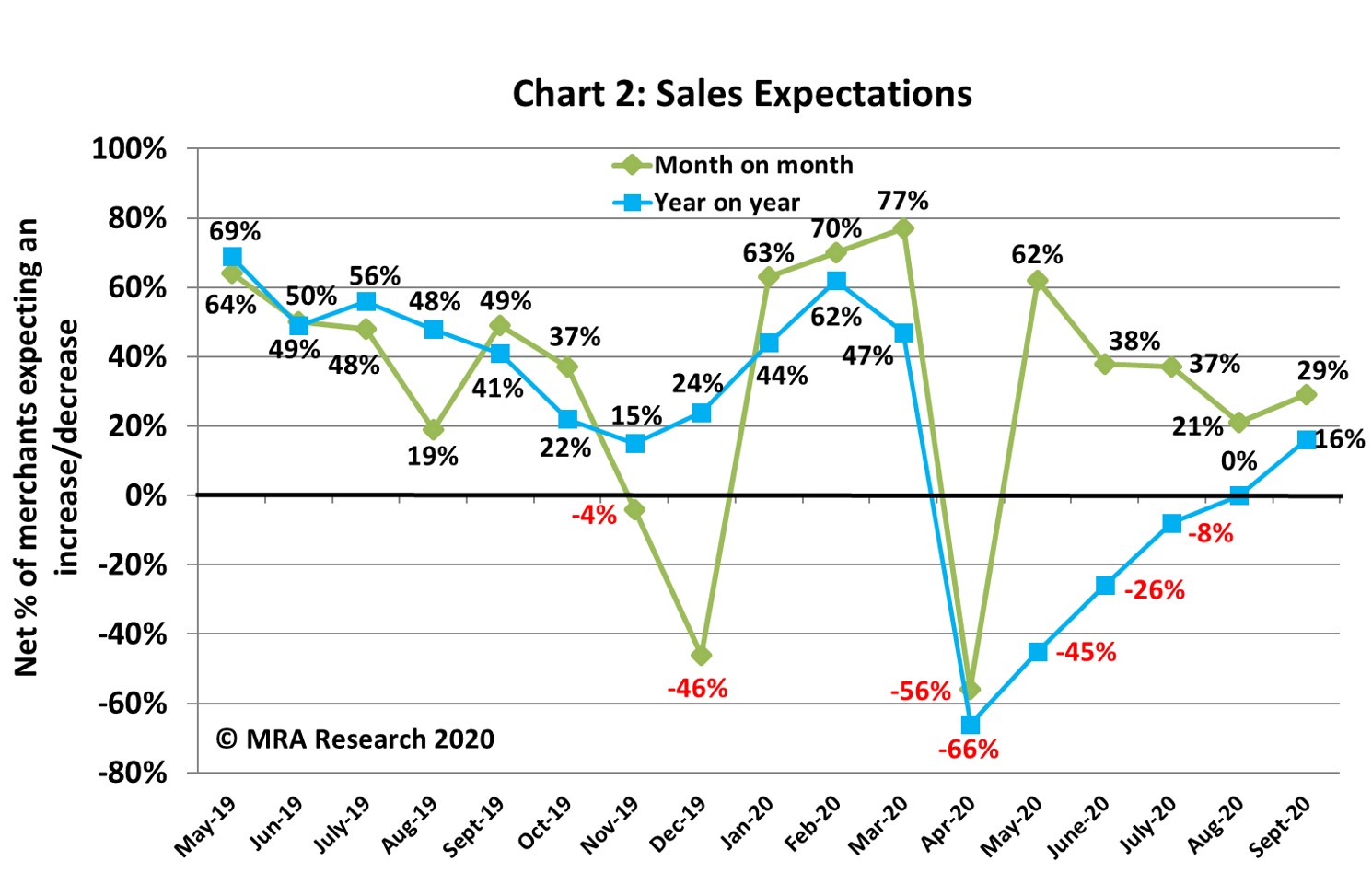

A net +29% of merchants expected sales to increase in September compared to August — see Chart 2. Sales expectations were broadly similar for merchants of all sizes and region.

While Independents overall expected no change month-on-month, Regional merchants and Nationals forecasted growth (+26% and +46% respectively).

Merchants’ year-on-year sales expectations indicate a continuing V-shaped recovery, with a net +16% forecasting an increase in September compared to the same period last year (also Chart 2).

Regionally, the picture was mixed. A net +36% of merchants in the Midlands and North expected to grow against just +3% of merchants in the South. A net -6% of merchants in Scotland expected sales to decline.

Quarter-on-quarter, sales expectations eased in September with only a net +10% of merchants predicting an improvement over the period. The outlook is similar for branches of all sizes. Merchants in the South (net +42%) and Nationals (+33%) are most positive.

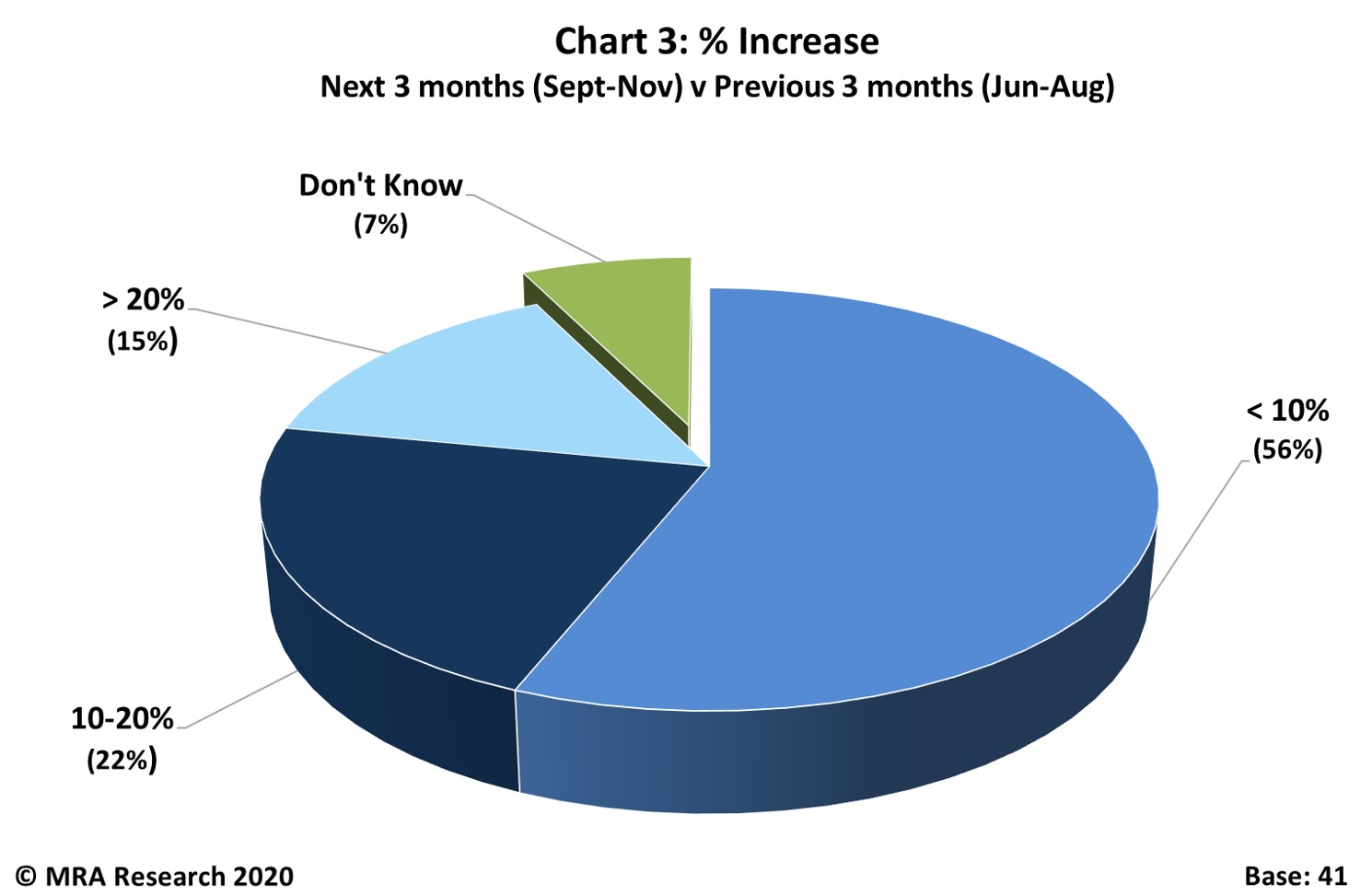

Of those expecting better sales in September to November, over half expect an increase of up to 10%. Just over one in five merchants expect growth of 10-20%. Some expect even stronger growth — see Chart 3.

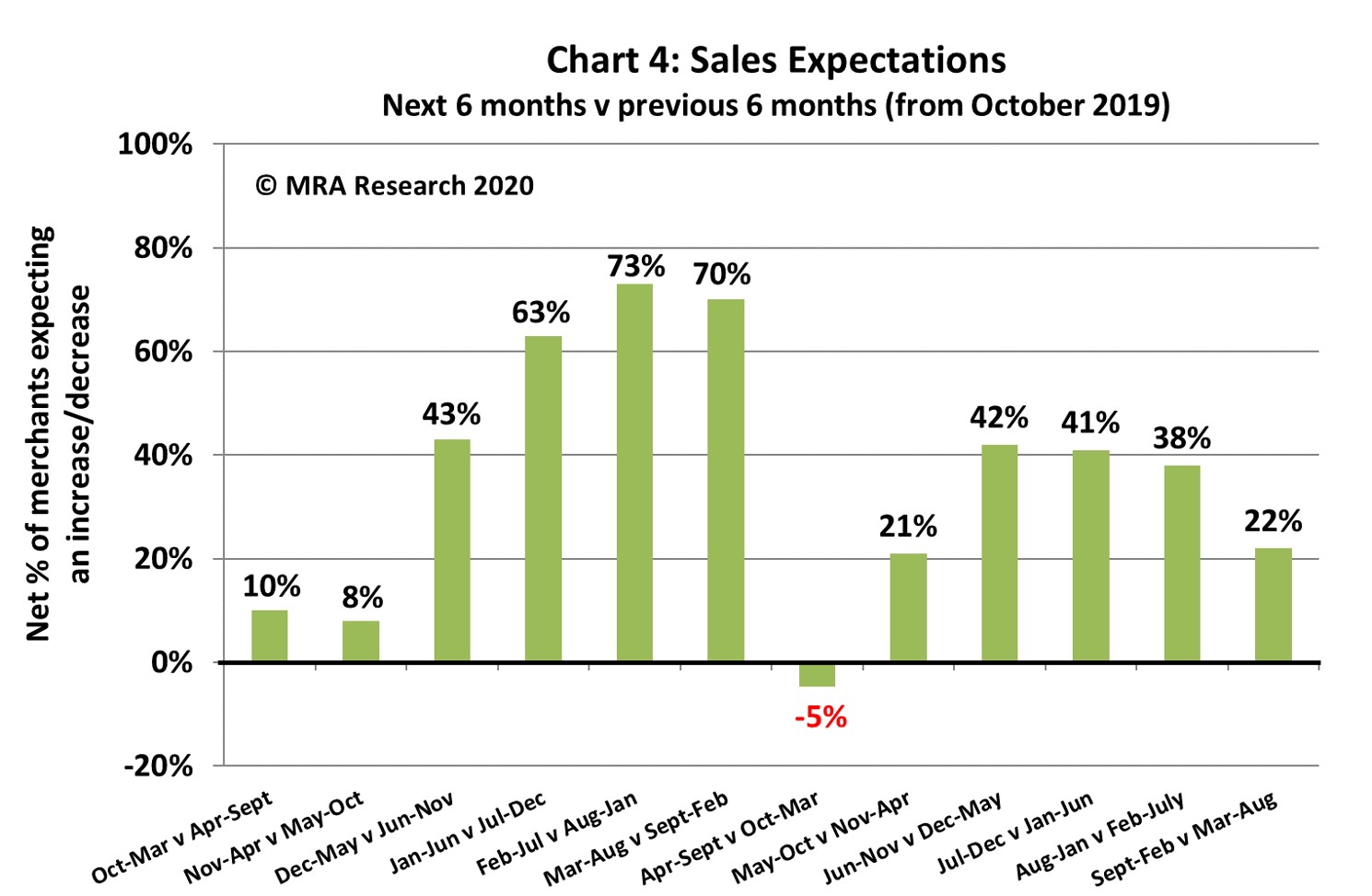

Looking six months ahead, while the outlook is positive — shown in Chart 4 — expectations are mixed. More small and large branches (net +32% and +28% respectively) forecast better sales over the period than mid-sized companies (+10%).

Regionally, merchants in the South are most confident (net +53%) compared to the North (+9%) and Scotland (+6%). A net -4% of merchants in the Midlands expect sales to drop.

Confidence in the market

Confidence in the market softened for the third consecutive month with a net +21% of merchants more confident in September compared to August.

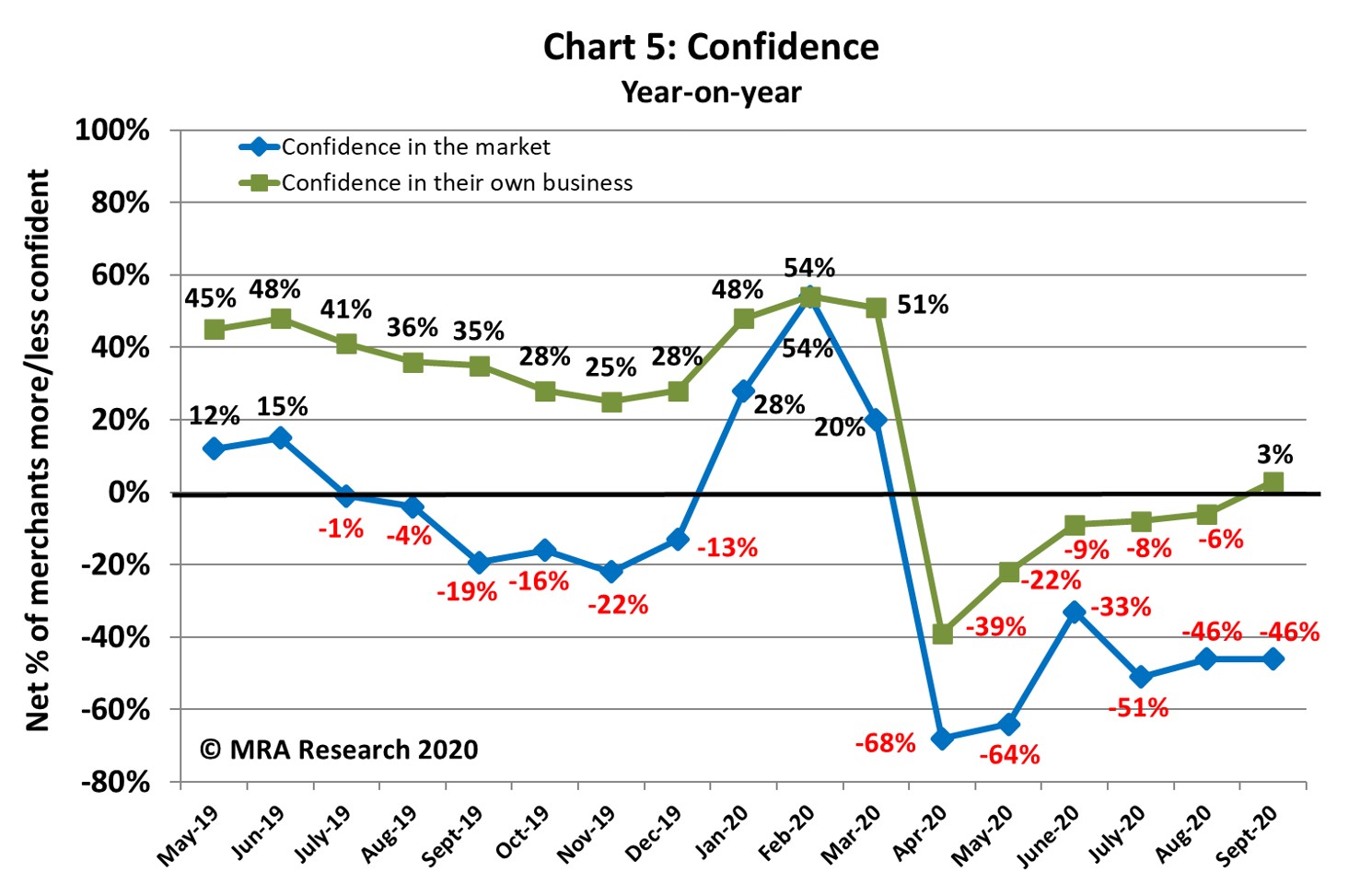

Compared to last year, confidence in the market has plateaued — see Chart 5. Recession and potential redundancies across the sector due to the pandemic were merchants’ main concerns.

Confidence in their business

Confidence in a merchants’ own business, however, continues to be strong with a net +48% more confident in September compared to August.

Year-on-year, merchants’ confidence in their own business continues to strengthen too, with a net +3% more confident over the period (also Chart 5).

About the Pulse

The Pulse is a monthly trends survey tracking builders’ merchants’ confidence and prospects over time. Produced by MRA Research, the insight division of MRA Marketing, it captures merchants’ views of future prospects in terms of sales expectations, confidence in their business, confidence in the market, and the key issues and problems they experience.

This report is the 17th in the series, with interviews conducted by MRA Research between 1-8 September 2020. Each month a representative sample of 100 merchants is interviewed. The sample is balanced by region, size and type of merchant, including nationals, regional multi-branch independents, and smaller independent merchants.

The full report can be downloaded from www.mra-research.co.uk/the-pulse or call Lucia Di Stazio at MRA Research on 01453 521621.