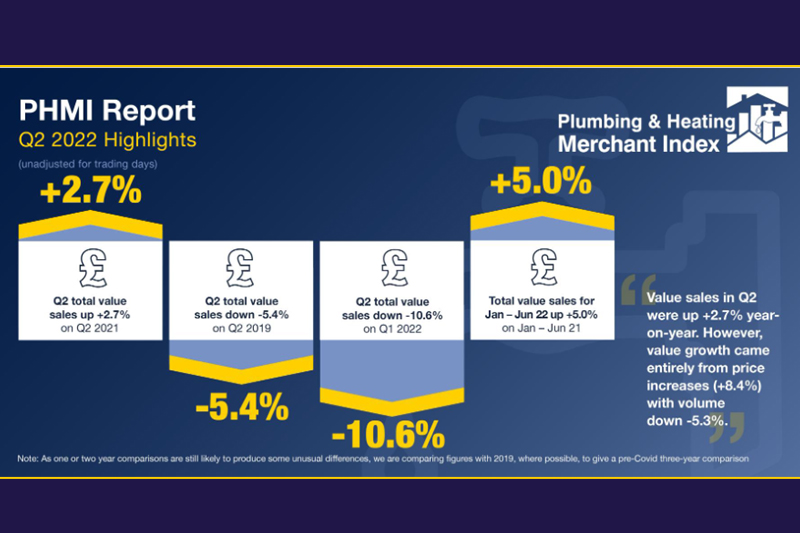

According to the latest Plumbing & Heating Merchant Index, value sales in plumbing & heating merchants during Quarter 2 2022 were +2.7% higher than in Quarter 2 last year, however, growth came mainly from higher prices (+8.4%) with volume sales down –5.3%.

Considering firstly the latest monthly data, June’s total plumbing and heating value sales – from over 70% of specialist Plumbing & Heating Merchants throughout Great Britain – were –4.0% lower than in June last year. Volume sales were down by –11.1% with price inflation of +8.0%. With two less trading days this year, like–for–like sales (which take trading day differences into account) were up +5.6%.

Compared with three years ago (taken a normal, pre-pandemic year as a benchmark), total value sales in June were –8.7% lower, with no difference in trading days.

Value sales in June were down –13.6% on May 2022 with volume –12.2% lower and prices down –1.6%. With one less trading day this month, like–for–like sales were down –9.2%. June’s PHMI index was 83.9, with one less trading day. The like–for–like index was 86.7.

Value sales in Quarter 2, meanwhile, were up +2.7% compared with the same three months last year. The increase again came entirely from +8.4% price inflation with volume sales –5.3% lower. With one less trading day this year, like–for–like sales were up +4.4%.

Looking back three years, value sales in Quarter 2 2022 were –5.4% lower than in Quarter 2 2019. With one less trading day this year, like–for–like sales were –3.8% lower.

Value sales in the second quarter of 2022 were –10.6% lower than in the first quarter. Volume sales were –8.9% lower and price

down –1.8%. With three less trading days in the most recent period Like–for–like sales were down –6.1%.

Overall value sales in January to June 2022 were +5.0% higher than in the same months a year earlier. Volume sales were –3.6% lower and prices were up +8.2%. With one less trading day so far this year Like–for–like sales were up +5.9%.

Overall value sales in January to June 2022 were –3.5% lower than in the same months in 2019. With one less trading day in the latest period, like–for–like sales were down –2.7%.

Value sales in the last 12 months were –0.6% lower than in July 2020 to June 2021. Volume sales were –7.5% lower and prices were up +7.4%. With two less trading days in the most recent period, like–for–like–sales were +0.2% higher.

Click here to view the full report.