As featured in the April edition of PBM, the latest installment of The Pulse shows that surging confidence levels and positive sales indications continue to be impacted by extended lead times and high prices.

This time last year, the country was in yet another lockdown so, not surprisingly, merchants were expecting sales in February 2022 to be considerably higher than the same month in 2021. Merchants’ expectations are also very strong for the next three months (February-April) and the next six months (February-July). Confidence in the market and in the prospects for their own business is also high.

However, long lead times and more price increases continue to affect merchant businesses, and merchants are concerned this will slow project completions and slow demand.

The Pulse, by MRA Research, is a monthly tracking survey of merchants’ confidence and prospects. Telephone interviewing took place between 1st and 3rd February 2022.

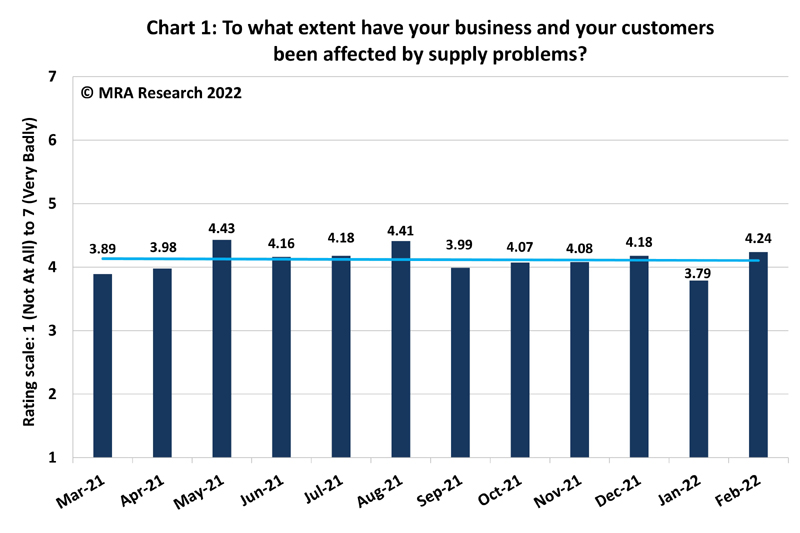

Materials supply

Supply problems got worse again in February after improving in January. Indeed, the average score (4.24) is the highest in six months — Chart 1. Exceptionally long lead times and surging prices continue to affect merchants.

Sales expectations

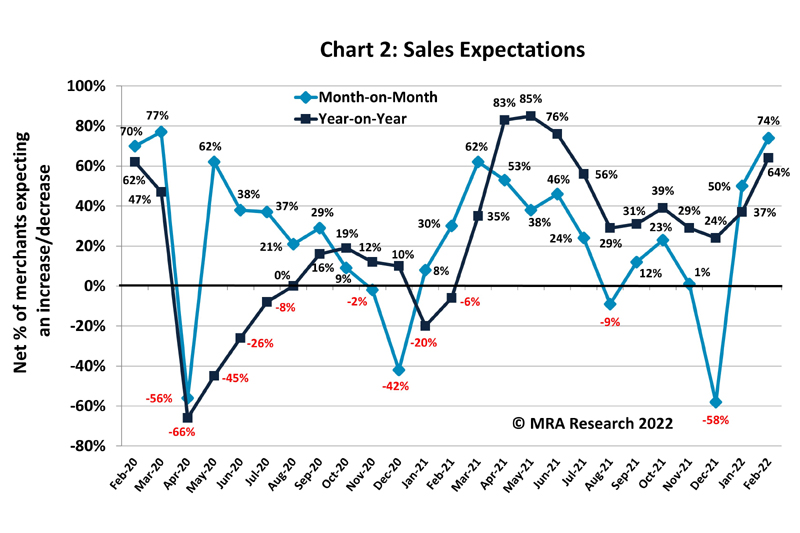

Merchants’ sales expectations rose again in February compared to January, with a net +74% of merchants expecting sales to improve over the period — Chart 2. Expectations were strong among merchants of all sizes and type, and in all regions.

Among merchants expecting sales to increase in February, 36% expected sales to grow by up to 9% compared with January, and 49% expected sales to increase by 10-20%. Eleven per cent expected sales to improve by more than 20%.

Year-on-year expectations were significantly higher in February (net +64%) compared to the same month in 2021, when the country was in lockdown — Chart 2. Expectations were strongest among Mid-sized outlets and merchants in the North (both +79%).

Among those expecting growth in February, compared to the same month in 2021, 40% expected growth of up to 9% and a further 37% expected growth of 10-20%. Nineteen percent expected more than 20% growth.

Quarter-on-quarter, merchants expect a very strong next three months, with nearly 8 in 10 (net +79%) expecting February-April sales to increase compared to the previous three months (November 2021 to January 2022). Expectations are strong across the board, and exceptionally high among Independent branches (+92%).

Among merchants expecting sales to grow over the next three months, over two in five expect sales to increase by up to 9%. A further 35% expect sales to grow by 10-20%, and nearly one in five expect sales to rise by more than 20%.

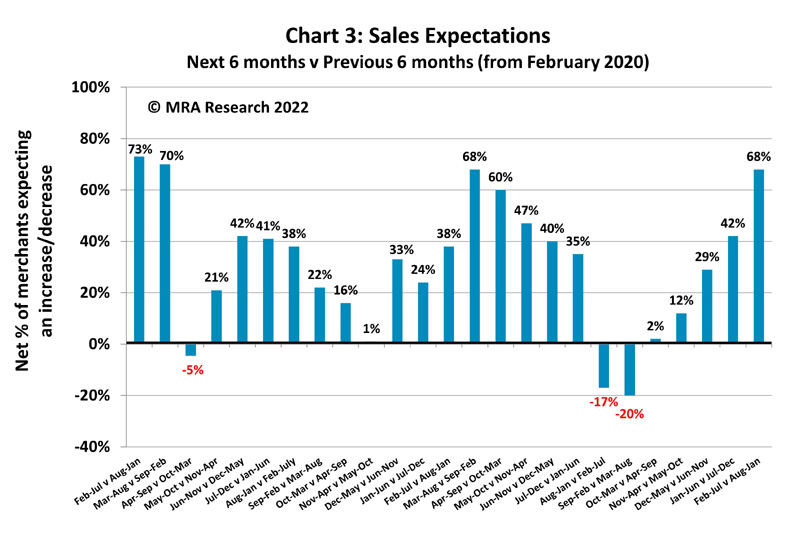

Over two thirds of merchants (net +68%) expect sales to grow in February-July compared to the previous six months (August 2021-January 2022) — Chart 3. Merchants in the South (+82%) had the strongest expectations.

Of merchants expecting growth over the next six months, just under half expect sales to increase by up to 9%. A further 31% expect sales to increase by 10-20%, and a further 15% expect sales to increase by up to 20% — Chart 4

Confidence in the market

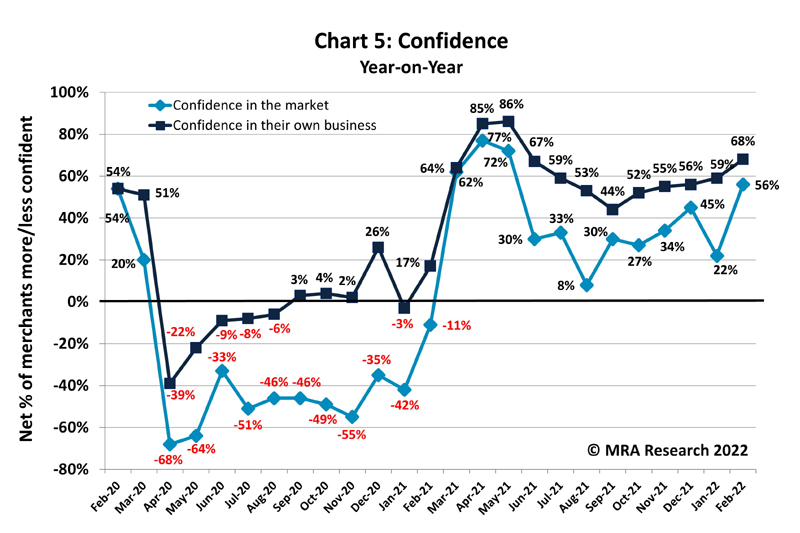

Compared with January’s survey (net +16%), month-on-month confidence in the market surged in February with a net +47% of merchants more confident. Confidence is strongest among merchants in the South (+71%).

Year-on-year confidence also improved significantly, with a net +56% of merchants more confident in February than the same month a year earlier — Chart 5. Confidence is particularly strong among merchants in the South (+79%). Confidence is weakest among branches in the North and Scotland (+26% and +29% respectively).

Confidence in their business

Merchants’ confidence in their own business strengthened considerably in February, with a net +69% more confident month-on-month than in January’s survey (+46%). Confidence is strongest among merchants in the South (net +92%).

Compared to the same month in 2021, merchants’ confidence in their own business continued to build on already high levels (+68%) — Chart 5. Merchants in the South (+87%) are most confident. Branches in the North are less so, but they are still confident (+26%).

The full report can be downloaded for free from www.mra-research.co.uk/the-pulse or call Ralph Sutcliffe at MRA on 01453 521621.

The difference between the percentage of merchants expecting growth and those expecting a decrease is the net figure, expressed as a percentage. A positive net percentage indicates growth, a negative indicates decline. Net zero implies no change.

About the Pulse

The Pulse is a monthly trends survey tracking builders’ merchants’ confidence and prospects over time. Produced by MRA Research, the insight division of MRA Marketing, it captures merchants’ views of future prospects in terms of sales expectations, confidence in their business, confidence in the market, and the key issues and problems they experience.

This report is the 34th in the series, with interviews conducted by MRA Research between 1st and 3rd February 2022. Each month a representative sample of 100 merchants is interviewed. The sample is balanced by region, size and type of merchant, including nationals, regional multi-branch independents, and smaller independent merchants.