Despite the difficulties, the BMBI is accentuating the positive and suggests an upturn may be in sight for the builders’ merchant sector.

Challenging market conditions continued to dominate the builders’ merchant sector during the the third quarter of 2024. However, figures released in the latest BMF Builders Merchants Building Index (BMBI) show the lowest level of quarterly decline since the start of 2023, which may herald a gradual return to growth.

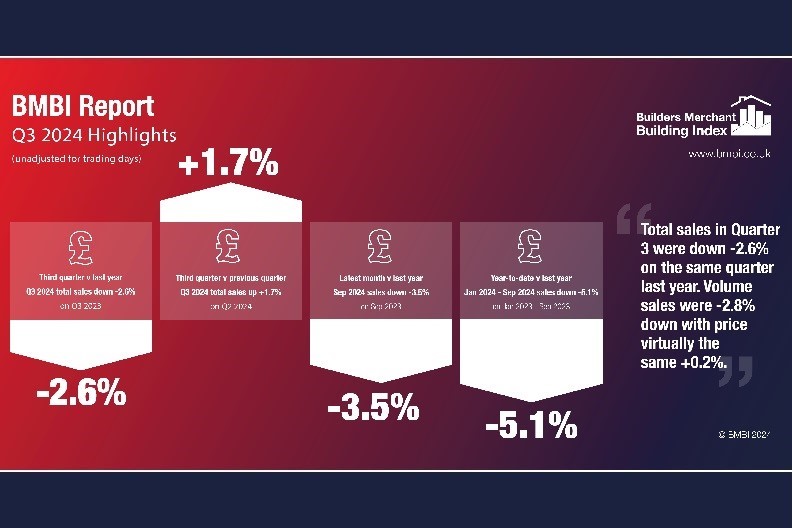

Quarter 3 2024 v Quarter 3 2023

Year on year total value sales in Q2 2024 fell by -2.6% compared with Q3 2023. Price growth was essentially at a standstill, increasing by +0.2%. Volume sales were down by -2.8%. With one more trading day in 2024, like-for-like total value sales were -4.1% lower this year.

Sales of the two largest categories fell by more than the total sales average. The largest, Heavy Building Materials saw value sales decline by -3.5%, with volume down by -3.9% and price growth of +0.4%. There were, however, product sector differences within this category, with larger than average declines for Bricks, Blocks, Insulation and Plasterboard, while Aggregates and Plaster bucked the trend, with sales increasing.

The other main category, Timber & Joinery Products, saw value sales decline by -4.8%, largely driven by Sheet Materials. However, timber performed better than expected, and Flooring & Flooring Accessories recorded growth.

Landscaping, the third largest category, saw a small decline in value sales (-0.3%). Kitchens & Bathrooms were down by – 6.1%, and Renewables and Water Saving was the weakest category, down by –29.1% in value. Four smaller categories, Decorating, Services, Tools and Workwear & Safetywear all saw growth, with the latter increasing +16.5% in value.

Quarter 3 2024 v Quarter 2 2024

Comparing sales in Q3 2024 with the previous quarter, shows ten out of twelve categories reporting sales value growth.

Total value sales in Q3 2024 were +1.7% higher than in the second quarter. Volume sales were +2.3% higher, whereas prices were -0.6% lower. With three more trading days in Q3 2024, like for like total value sales were +3.0% higher than the previous quarter.

The two largest categories, Heavy Building Materials and Timber & Joinery both saw value sales increase by +3.2%. Landscaping, however, was the weakest category, down -9.3%.

Year-to-date 2024 v last year (January – September 2024 v January – September 2023)

Comparing the first three quarters of this year with the same period in 2023, shows total merchants value sales from January to September 2024 were -5.1% lower than the same period a year earlier. Volume sales were -6.1% lower, while prices were +1.1% higher. With two more trading days in the latest 12-month period, like for like value sales were -6.1% lower.

Five of the smaller categories sold more, led by Workwear & Safetywear (+14.5%) and Tools (+6.0%), but the two largest categories Heavy Building Materials (-7.0%) and Timber & Joinery Products (-7.5%) were amongst the weakest.

Commenting on the data, Emile van der Ryst, Senior Client Insight Manager – Trade at GfK said: “The builders’ merchant sector continued to struggle in Q3, as part of the wider economy, influenced by uncertainty of the direction taken by the new government, and continuing global tensions. The remainder of the year will continue to be challenging; however, merchants are noting the first signs of positive sentiment, which means the sector could start returning to growth in the second half of 2025.”

BMF CEO John Newcomb added: “Although the second half of the year has seen a stronger pipeline of new orders in some areas of construction, new housing and domestic RMI – the cornerstone of the merchant market – has remained flat. A strong housing sector would deliver the widest economic and growth benefits across the UK, and we await government plans to stimulate this market in 2025 and beyond.”

Mike Rigby, MD of MRA Research who produce this report, said: “There was a small increase in Total Merchant value sales quarter-on-quarter, but sales were down year on year. The new Labour government swept into power on high expectations and a desire for change as voters responded to the promise of growth. But a wet summer and a series of gloomy pronouncements about growth-postponed quickly knocked the stuffing out of consumers’ confidence and talked down the markets.

“GfK’s long running Consumer Confidence Index fell to -21 in October, the lowest it has been since March. Perhaps the most telling metric was people’s sentiments about the general economic situation over the last 12 months, which dropped -5 points to -42. A YouGov poll after the budget statement confirmed that 39% of respondents thought the budget would leave them and their family worse off. This isn’t great news for the RMI market as people will be more inclined to save than spend.”

Mike added: “It is good news that the government wants to grow the economy over the course of this parliament. The building industry looks forward to that, and to the necessary improvements in the planning regime, to rebuilding 500 schools, extending HS2 to London Euston, and building 1.5 million homes and some new towns.

“But you can’t just announce growth and expect it to happen just like that. The industry wound down and mothballed capacity to meet reduced demand. And it isn’t going to invest in new capacity without some certainty of government steadfastness and expectations of demand over a longer time horizon. £100m-£200m factories can take years to take through planning and get built and connected to the grid and water services. More than that, we don’t have the skilled people to build all those homes.”

The Builders Merchant Building Index (BMBI) report contains data from GfK’s Builders Merchants Panel, which analyses data from over 80% of generalist builders’ merchants’ sales throughout Great Britain. The BMBI, a brand of the BMF, is produced and managed by MRA Research.

GfK’s Builders’ Merchant Point of Sale Tracking Data sets a gold standard in reliable market trends. Unlike data from sources based on estimates, or sales from suppliers to the supply chain, this up-to-date data is based on actual sales from merchants to builders and other trades.

More information can be found at www.bmbi.co.uk