Despite a fall in total value sales during the final quarter of 2024, the figures released in the latest BMF Builders Merchant Building Index (BMBI) “provide positive signals for the year ahead.”

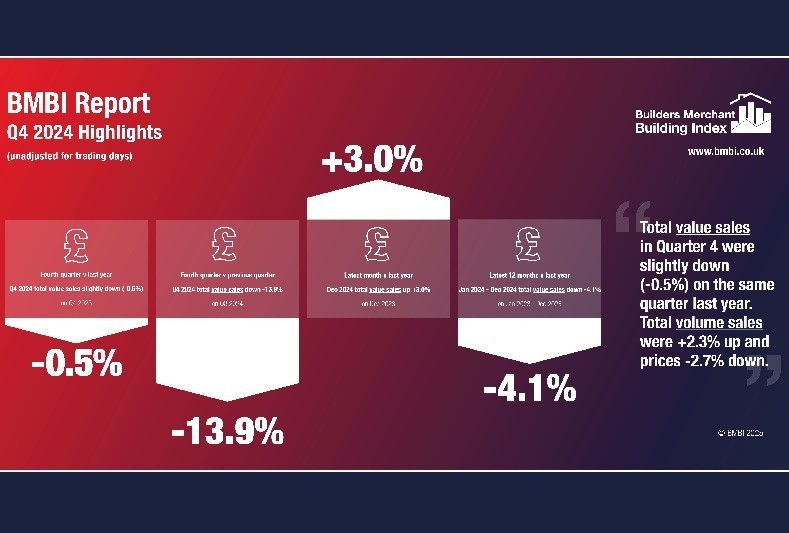

The latest Builders Merchant Building Index (BMBI) report reveals builders’ merchants’ value sales for Q4 2024 were down -0.5% compared to Q4 2023, as an increase in volume sales (+2.3%) was countered by a fall in prices (-2.7%). With one additional trading day in Q4 2024, like-for-like value sales (which take the number of trading days into account) were -2.2% lower.

Four of the twelve categories sold more in Q4 2024, led by Tools (+8.8%). Value sales of the two largest categories – Timber & Joinery Products (-2.6%) and Heavy Building Materials (-0.2%) – were down year-on-year. Renewables & Water Saving (-8.9%) was the weakest category.

Quarter-on-quarter builders’ merchants’ value sales for Q4 2024 were -13.9% lower than the previous three-month period. Volume sales tumbled -15.6%, while prices were slightly raised (+2.0%). Value sales in just three categories were up compared to Q3 – these were Plumbing Heating & Electrical (+2.7%), Workwear & Safetywear and Renewables & Water Saving (+1.5%). Seasonal category Landscaping (-30.9%) was the weakest. With four less trading days in the most recent period, like-for-like value sales were down -8.2%.

Quarter 4 total value sales were given a boost by December sales, which were up +3.0% year-on-year. Volume sales climbed +7.4%, while prices fell -4.1%. Seven of the twelve categories sold more in value sales, led by Landscaping (+15.9%), Services (+8.8%), Tools (+8.6%) and Heavy Building Materials (+3.9%). Timber & Joinery Products (+0.1%) was flat.

December value sales were weak compared to November (-32.5%) but this is in line with seasonal trends.

Total value sales for January to December were -4.1% lower than the same period in 2023. With three more trading days this year, like-for-like value sales were down -5.2%. Volume sales for 2024 were down -4.3% compared to last year, and prices were largely inline (+0.2%).

Five of the twelve categories sold more in value, with Workwear & Safetywear (+10.8%), Tools (+6.7%) and Services (+3.0%) faring the best. Renewables & Water Saving (-24.0%), Timber & Joinery Products (-6.4%) and Heavy Building Materials (-5.5%) were weakest.

“If Merchants are to earn a bigger slice of the pie, particularly while trading conditions remain tough, they may need to shake up their approach to engage with the way modern consumers – including trades and end users – want to buy.”

John Newcomb, CEO of the BMF, commented: “After two pretty tough years, I remain cautious about overstating prospects for the coming year, but one or two encouraging signs are now emerging in our sales data. With interest rates gradually coming down and consumer confidence improving, we should be preparing for growth in the second half of 2025.”

Emile van der Ryst, Key Account Manager – Trade & DIY at NiQ GfK, added: “There is clear evidence that the builders’ merchants sector turned a corner as 2024 came to a close. The most positive indicator has been a return to volume growth, with Q4 2024 up by +2.3% against Q4 last year. Coupled with this, price growth was negative for the first time in years. Positivity around sentiment continues to grow, with this acting as a reference point for anticipated future growth.”

Meanwhile, Mike Rigby, MD of MRA Research who produce this report, provided an in-depth commentary. He said: “The latest GB construction data from ONS shows a slight increase (+0.5%) in output in Q4 despite a -0.2% fall in December, and overall a modest +0.4% increase in output for 2024 compared to 2023. While this is the fourth consecutive year of annual growth, it may not feel like it for Merchants who were actually down -4.1% on value sales year-on-year.

“Whether things change for the better in 2025 will hinge on a number of factors, including restoring consumer confidence to encourage spending on property and home improvement projects. Inflation may have dropped to 2.5% in December and there was also a cut to interest rates, but prices and outgoings are still considerably higher than they were pre-Ukraine war, putting continued pressure on household budgets.”

Mike continued: “The latest Consumer Confidence Index from NIQ GfK shows a drop in all metrics at the turn of the year with the biggest drops being to people’s perception of the general economic situation over the next 12 months (-8). January’s overall index fell -5 points to -22 – the lowest it has been in over a year.

“Changing hearts and minds about how and where consumers spend their limited disposable income may require a change of tack. A report into what matters to today’s consumers, published by Capgemini Research Institute, showed that the cost-of living crisis was still driving people to seek out more affordable options and that sustainability was a critical factor in the purchasing decisions for 64% of those surveyed. Social media is an increasingly influential factor, particularly for Gen Z consumers.

“Interestingly, generative AI is now influencing more buying decisions with 58% of people choosing GenAI recommendations over traditional search engines. Demand for quick delivery has also surged.”

Mike concluded: “If Merchants are to earn a bigger slice of the pie, particularly while trading conditions remain tough, they may need to shake up their approach to engage with the way modern consumers – including trades and end users – want to buy.”

The Q4 2024 BMBI report is available to download at www.bmbi.co.uk

The Builders Merchant Building Index report contains data from NiQ GfK’s ground-breaking Builders Merchants Panel, which analyses data from c.88% of generalist builders’ merchants’ sales throughout Great Britain (including national, multi-regional and regional merchants such as Jewson, Travis Perkins, Huws Gray, EH Smith, Gibbs & Dandy, MKM, Bradfords, Covers and Sydenhams). The BMBI, a brand of the BMF, is produced and managed by MRA Research.

NiQ GfK’s Builders’ Merchant Point of Sale Tracking Data “sets a gold standard in reliable market trends.” Unlike data from sources based on estimates, or sales from suppliers to the supply chain, this up-to-date data is based on actual sales from merchants to builders and other trades.

More information can be found at www.bmbi.co.uk