The RICS UK Construction & Infrastructure Monitor for Q3 2022 reveals that construction activity is expected to continue to slow with credit constraints, labour and material shortages all impacting growth.

The Royal Institution of Chartered Surveyors (RICS) UK Construction & Infrastructure Monitor for Q3 2022 indicates that construction activity is expected to slow over the next 12 months. It reveals that while workloads are still rising, growth is starting to decline and expectations for the next 12 months are now also not as positive as were recorded in this survey in the previous quarter. The RICS also says that, significantly, there is now greater concern regarding how macro factors may impact the industry, specifically with respect to credit constraints.

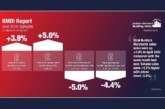

The headline reading of construction workload activity for the whole of the industry has lost momentum over the past quarter, with a net balance of +17% of respondents reporting an increase, compared to +30% in Q2. The infrastructure sector is continuing to hold up better than other areas; with a net balance of +32% this quarter. However, momentum has slowed across all categories. Private industrial, for example, dropped from a net balance of +28% in the previous quarter to +12% in this quarter and private commercial dropped from +25% to +10%.

For private residential, the latest workloads net balance slipped to +17%, compared to a reading of +29% beforehand.

In terms of business enquiries, for either new projects or contracts, these have also eased compared to Q2. In Q2 net balance was at +36% however, this quarter it’s fallen to +15%. This underlines the other metrics showing that the market is losing some steam, as does the fact that profit margins are also under increased pressure.

Expectations from contributors fell to a net balance of -23% this quarter from -14% in Q2; the worst figure in two years. Turbulent economic conditions, including the rise in interest rates and inflation both domestically and internationally is impacting across the market.

There are several difficulties facing the industry, and respondents cited shortages in materials and labour, alongside increasing financial constraints. 77% of contributors cite material and labour shortages while 74% drew attention to a scarcity of labour as factors hindering activity. Also, 56% of respondents cited a lack of quantity surveyors as a key factor holding back construction activity.

Simon Rubinsohn, Chief Economist at RICS, said: “The deteriorating macro environment is clearly taking a toll on the construction industry with access to credit now being cited as a key challenge for businesses alongside the more familiar issues around building materials and labour. Indeed, the RICS metric capturing the extent of skill shortages in the sector has barely budged in recent quarters with quantity surveyors and a range of skilled trades in particular short supply.

“Meanwhile, the impact of the shift in the economic outlook is most visible in the residential and commercial sectors where workloads are now viewed as likely to flatline over the coming year. Ongoing commitments to a number of big projects is, however, continuing to support activity in the infrastructure area. The thoughts of the Chancellor on November 17th may provide some clues as to whether this trend is likely to be sustained over the longer term.”

For more information and to view the report, visit www.rics.org/uk