Latest S&P Global UK Construction PMI reveals subdued construction sector performance continued in June.

UK construction companies recorded further sharp declines in output and new orders during June. However, both rates of contraction eased from May’s six-year records. Furthermore, cost pressures moderated in June and supply chain disruptions were notably less acute than in April and May.

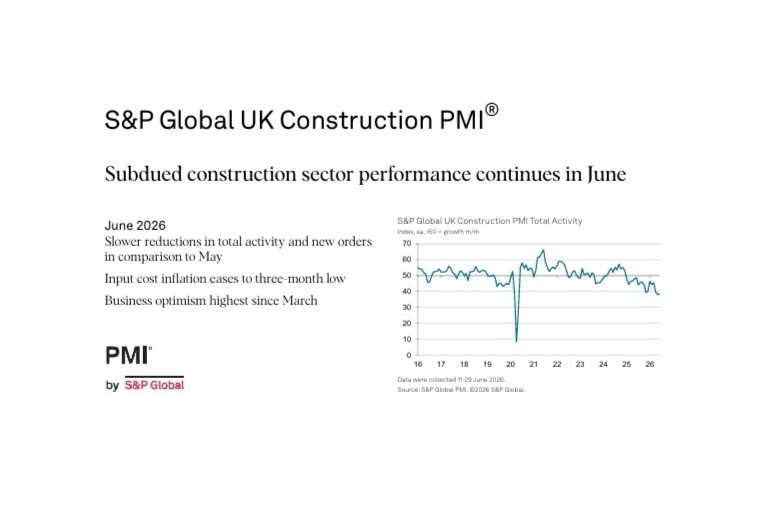

The seasonally adjusted S&P Global UK Construction Purchasing Managers’ Index™ (PMI®) — an index tracking changes in total industry activity — registered 38.4 in June, up slightly from May’s six-year low of 38.2 but still well below the neutral 50.0 value. Construction output has decreased in each month since January 2025 and the latest fall was the second fastest since the start of the pandemic.

Commercial construction was the best-performing category and showed some resilience in June (index at 41.5). It was also the only segment to record a slower downturn in activity than in the previous month. House building activity (index at 35.9) decreased at the sharpest pace in 2026 to date. Meanwhile, civil engineering activity fell to the greatest extent since April 2020 (index at 22.1).

Lower levels of construction activity were attributed to a mixture of subdued housing market conditions, higher borrowing costs, elevated business uncertainty, and delayed project starts. June data signalled another sharp fall in total new work, although the speed of the downturn was the slowest since March.

Anecdotal evidence cited factors such as fewer new build house sales, weak business investment spending, and intense competition for new orders. Some firms commented on improved opportunities to tender for defence and energy sector projects.

“Twice as many construction companies (38%) expect an increase in business activity over the year ahead as those that predict a decline (19%). This pointed to a marked rebound in business optimism from the six-month low seen in May.”

Cutbacks to employment numbers continued across the construction sector in June. This marked 18 months of sustained job shedding. Moreover, subcontractor usage fell sharply. This contributed to the fastest improvement in subcontractor availability since April 2025.

Demand for construction products and materials softened again in June, which helped to alleviate pressures on supply chains. Survey respondents also noted rising inventories among vendors and fewer instances of shipping delays.

Measured overall, supplier performance deteriorated to the least marked extent since March. Average cost burdens increased sharply in June. Higher raw material prices, staff wages and transport bills were widely reported in June. Around 53% of the survey panel reported a rise, while only 1% signalled a reduction.

However, the resulting seasonally adjusted index pointed to the slowest pace of inflation for three months. Twice as many construction companies (38%) expect an increase in business activity over the year ahead as those that predict a decline (19%). This pointed to a marked rebound in business optimism from the six-month low seen in May. However, confidence remained much weaker than the long-tun survey average.

Positivity was often linked to forthcoming public sector projects and greater infrastructure spending, alongside the restart of delayed projects.

Comment from Tim Moore, Economics Director at S&P Global Market Intelligence:

“The downturn in UK construction output lost some intensity in June amid a softer reduction in commercial building work. House building and civil engineering activity nonetheless registered sharper declines than in May, with the latter seeing its weakest performance since the start of the pandemic.

“New work decreased to the least marked extent since March, despite widespread reports of challenging market conditions. Construction companies commented on headwinds from subdued housing sales, elevated interest rates and squeezed consumer finances, alongside cutbacks to business investment plans. Some firms noted delays with infrastructure work and fewer public sector tender opportunities, but energy markets were cited as an area of positivity.

“Supply chain challenges appear to have receded, with vendor delivery times lengthening to the smallest degree since March. Construction companies also reported a slowdown in input price inflation from the near four-year peak seen in May.

“June data indicated a recovery in business activity expectations across the construction sector since May, although confidence levels remain well short of historic trends. A number of survey respondents suggested recent new contract awards and an expected improvement in broader market conditions had underpinned optimism.”