The latest IHS Markit / CIPS Construction PMI for September 2021 shows that shortages of materials and staff are continuing to hold back the construction recovery.

September data revealed another growth slowdown in the construction sector, with output volumes rising to the smallest extent for eight months. This partly reflected softer demand conditions than the peak seen earlier in the summer. Survey respondents also cited disruptions on site from unavailable transport, a severe lack of materials and continued staff shortages.

A rapid drop in sub-contractor availability was reported in September. Imbalanced demand and supply contributed to the steepest rise in sub-contractor charges since the survey began in April 1997. Some firms noted that the unpredictable pricing environment had slowed clients’ decision-making on new orders and led to delays with contract awards.

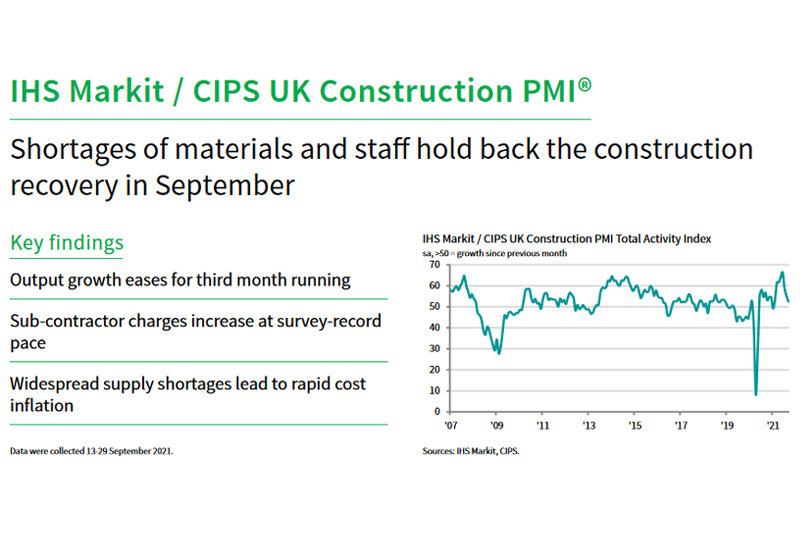

At 52.6 in September, down from 55.2 in August, the headline seasonally adjusted IHS Markit/CIPS UK Construction PMI Total Activity Index dropped further below the 24-year high seen in June (66.3). The latest reading signalled only a moderate expansion of total construction output and the weakest speed of recovery for eight months. Reports from survey respondents linked the slowdown to a combination of supply chain issues and softer demand.

All three broad categories of construction activity saw a loss of momentum in September, with the biggest slowdown seen in civil engineering (51.0, down from 54.8 in August). House building also decelerated in September, with the latest expansion the weakest since the recovery began in June 2020 (52.8). This left the commercial segment (53.6) as the best-performing category during September. Resilience in this sub-sector reflected a continued boost to order books from the reopening of the UK economy.

Construction companies recorded a moderate increase in new work during September, with the rate of growth easing sharply to its weakest since the start of 2021. The slowdown was linked to hesitancy among clients and less favourable demand conditions.

September data indicated another strong rise in employment numbers across the construction sector, driven by greater

workloads and stretched business capacity. However, the latest rise in staffing levels was the least marked since April,

which partly reflected long wait times to fill vacancies.

A lack of sub-contractor availability added to the squeeze on labour supply in September. Shortages of sub-contractors also led to additional cost pressures, with rates charged for sub-contracted work increasing at a survey-record pace. Purchase prices increased rapidly in September, although the rate of inflation eased further from June’s all-time peak.

Around 78% of the survey panel reported a rise in their cost burdens, which was mostly linked to supply shortages and transport surcharges. Meanwhile, the latest survey illustrated that construction firms remained highly upbeat about the business outlook. Just over half (51%) forecast rising output, while only 8% anticipate a decline. However, the degree of confidence was weaker than August amid some concerns that the supply chain crisis will hinder growth.

Data were collected 13-29 September 2021.

Tim Moore, Director at IHS Markit, which compiles the survey said:

“September data highlighted a severe loss of momentum for the construction sector as labour shortages and the supply chain crisis combined to disrupt activity on site.

“The volatile price and supply environment has started to hinder new business intakes as construction companies revised cost projections and some clients delayed decisions on contract awards. As a result, the latest survey data pointed to the worst month for order books since January’s lockdown.

“Shortages of building materials and a lack of transport capacity led to another rapid increase in purchase prices during September. There was also a considerable decline in the availability of sub-contractors, with survey respondents citing shortages of bricklayers, drivers, groundworkers, joiners, plumbers and many other skilled trades. Measured overall, prices charged by sub-contractors increased at the fastest rate since the survey began in April 1997.”

Duncan Brock, Group Director at the Chartered Institute of Procurement & Supply, said:

“Construction activity suffered another setback in September, as builders were hammered by staff and material shortages, delivery delays and higher business costs as this phase of the post-pandemic recovery became the shakiest for eight months.

“Housing and civil engineering bore the brunt of the slowdown with residential building the weakest since June 2020 during the early stages of the pandemic. The increases in shortages also affected project agreements with a sharp fall in new order growth, where customers hesitated to commit, uncertain about prices and the timing of completion. Over 60% of supply chain managers said their deliveries were taking longer and 78% were paying more for their goods as inflation remained stubbornly high.

“Good news for job seekers though as the demand for skilled labour remained unabated, and companies were left wanting more. Sub-contractors were unable to fill the widening gap of need as their availability shrank and prices charged accelerated to record levels. Unless stronger supply chain performance is nailed down along with headcount, we are heading towards a stagnant autumn because the sector is certainly not on an even footing at the moment.”

Related news

UK Construction PMI for August 2021

UK Construction PMI for July 2021

UK Construction PMI for June 2021

UK Construction PMI for May 2021

UK Construction PMI for April 2021