The S&P Global / CIPS UK Construction PMI report for July signalled a renewed expansion of overall construction output, following the marginal decline seen during the previous month.

This was led by the strongest rise in commercial building since February and another solid contribution to growth from civil engineering activity. However, the latest data signalled another sharp reduction in residential construction activity.

Survey respondents widely noted that higher interest rates and the uncertain UK economic outlook had constrained order books in July. Softer demand and fewer supply bottlenecks in turn led to the fastest improvement in vendors’ delivery times since March 2009.

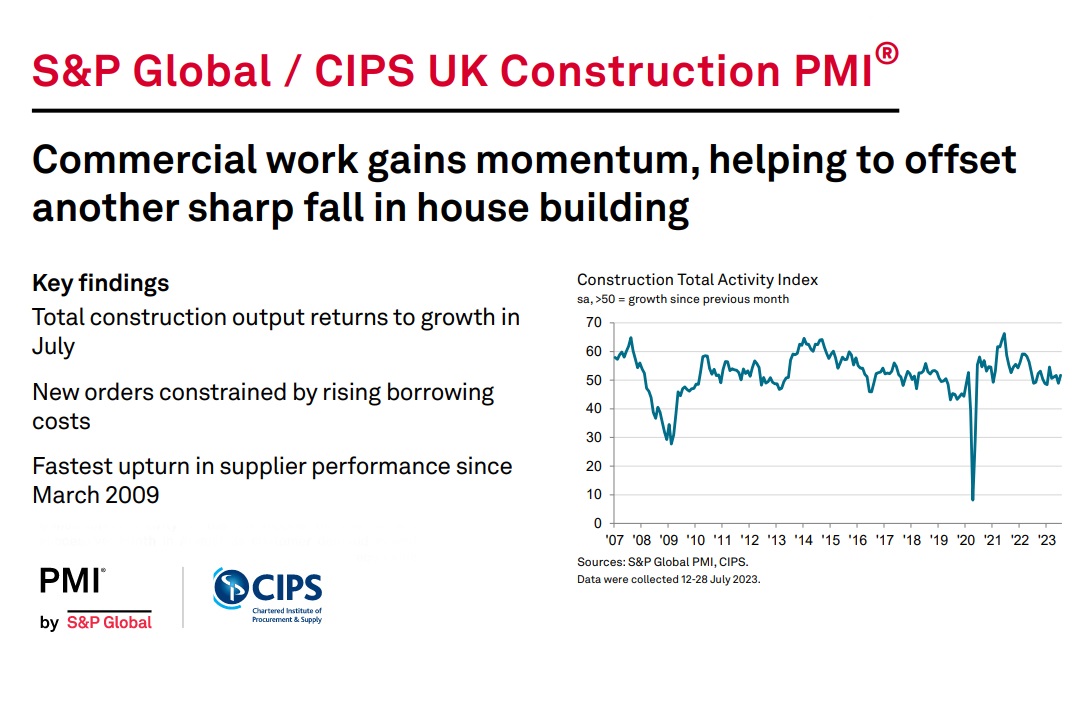

The headline S&P Global / CIPS UK Construction Purchasing Managers’ Index (PMI) – a seasonally adjusted index tracking changes in total industry activity – posted 51.7 in July, up from 48.9 in June and the highest level for five months. Notwithstanding, the latest reading signalled only a moderate rise in overall construction output.

Robust increases in commercial building (index at 54.4) and civil engineering (53.9) were offset by a steep fall in house building (43.0). Lower volumes of residential work have now been recorded for eight consecutive months, although the rate of decline eased to its least marked since April.

Construction companies noted that rising borrowing costs had led to fewer sales enquiries and slower decision-making among clients in July. The latest survey pointed to only a marginal rise in total new work and the rate of growth was slower than seen on average in the first half of 2023. Some firms cited solid demand for refurbishment projects and greater opportunities for infrastructure work.

Staff hiring was a relatively bright spot in July, with the pace of job creation accelerating to its strongest since October 2022. Higher levels of employment have now been recorded in each of the past six months. Some firms noted that improved candidate availability was a factor encouraging them to boost their workforce numbers, while others typically cited long-term business expansion plans.

July data indicated weaker demand for construction inputs. Purchasing activity has now decreased in each of the past two months, which reflected destocking efforts alongside subdued order books. A combination of lower demand and rising material availability contributed to a sharp improvement in supplier performance. Latest data illustrated that lead times shortened to the greatest extent for nearly fourteen-and-a-half years.

Some survey respondents suggested that increased competition among suppliers had helped to support more favourable price negotiations. However, there were also reports that elevated general inflation and higher wage costs continued to push up purchasing prices. Measured overall, average cost burdens increased moderately in July and at a much softer pace than seen on average in the first half of 2023.

Finally, business activity expectations for the year ahead remained positive overall in July and picked up slightly since the previous survey period. Reports from construction companies nonetheless indicated that pressure on customer budgets from higher interest rates remained a key factor holding back output growth projections for the next 12 months.

Tim Moore, Economics Director at S&P Global Market Intelligence, which compiles the survey said:

“July data indicated that some parts of the UK construction sector gained momentum, notably commercial building and civil engineering activity. This led to a renewed rise in total construction output which, although modest, was the fastest for five months. Survey respondents commented on increased infrastructure work, office refurbishments, and resilient demand for a range of commercial projects.

“Meanwhile, another steep reduction in house building acted as a severe constraint on construction growth. Around 35% of the survey panel reported a decline in residential work during July, while only 18% signalled a rise. Lower volumes of housing activity have been recorded in each month since December 2022, with construction companies widely reporting subdued sales due to rising interest rates and worries about the economic outlook.

“Supply conditions improved considerably in July, as a combination of weaker demand and replenished stocks meant that delivery times shortened to the greatest extent since 2009. As a result, input prices inflation was much lower than seen on average in the first half of the year, but there were still many reports from construction firms that higher wages costs had put upward pressure on business expenses.”

Dr John Glen, Chief Economist at the Chartered Institute of Procurement & Supply, said:

“Although the sector showed a slight uplift in activity in July, there is a question mark over the sustainability of this growth and the challenges that lie beneath the floorboards.

“Decisions about buying a new home are being delayed by many consumers. Another fall in residential building levels and for the eighth month in a row, it’s obvious that UK interest rate rises and cost of living pressures have dealt a hammer blow to the housing sector. The commercial and civil engineering sectors remained the only engines of growth last month.

“For those that secured additional work, the best improvement in delivery times for raw materials since March 2009 will be music to their ears as supply chain disruptions improved and shortages lessened. Likewise the right skilled candidates found the best positions as job creation rose to the highest for nine months so there were some bright spots in the data.

“In spite of more uncertainty and thinner margins, builders kept their confidence up and focussed on resilience in their operations as optimism about the next 12 months remained fairly steady.”

Related News

S&P Global / CIPS UK Construction PMI June 2023 data

S&P Global / CIPS UK Construction PMI May 2023 data

S&P Global / CIPS UK Construction PMI April 2023 data

S&P Global / CIPS UK Construction PMI March 2023 data

S&P Global / CIPS UK Construction PMI February 2023 data

S&P Global / CIPS UK Construction PMI January 2023 data

S&P Global / CIPS UK Construction PMI December 2022 data

S&P Global / CIPS UK Construction PMI November 2022 data

S&P Global / CIPS UK Construction PMI October 2022 data