The latest IHS Markit / CIPS Construction PMI data, for February, indicated that business activity gained momentum across the UK construction sector.

Indeed, building companies commented on the strongest rise in output since mid-2021 amid stronger client confidence and work on new projects commencing. However, construction companies continued to report widespread supply constraints and rapidly increasing input costs, though the rate of inflation in the latter was the least severe for 11 months.

That said, the report showed that ongoing disruption dampened the year-ahead outlook for activity, with confidence at the lowest since January 2021.

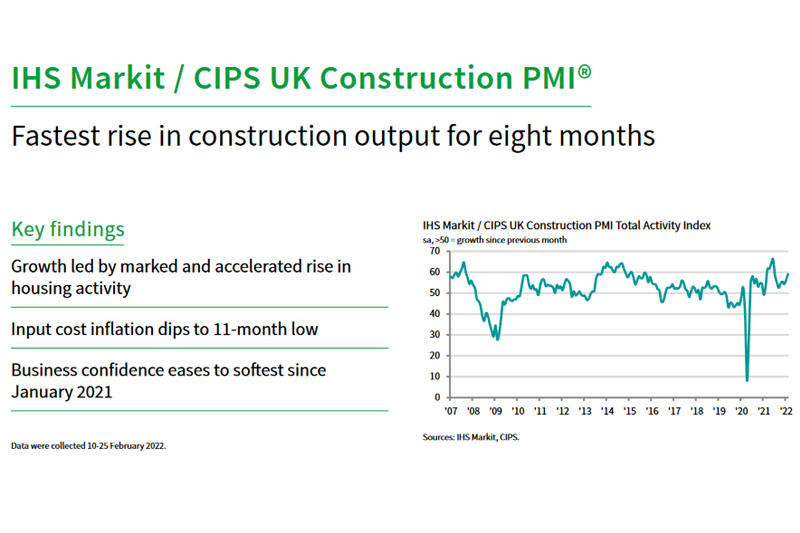

The headline seasonally adjusted IHS Markit/CIPS UK Construction PMI Total Activity Index registered 59.1 in February, up from 56.3 in January to signal a robust and accelerated rise in output volumes. The headline index has now posted above the neutral 50.0 threshold in each of the last 13 months.

House building (index at 61.5) replaced commercial work (58.4) as the best performing category of construction work in February. The latest increase in residential work was the strongest for eight months. Commercial construction also expanded at a quicker pace than in January, with the rate of growth the sharpest since last July. Meanwhile, civil engineering activity (index at 57.5) increased at an accelerated pace that was the strongest since June 2021.

New order growth accelerated for the fourth month running in the latest survey period to extend the current sequence of expansion to 21 months. Moreover, the rate of growth was the fastest since last August as construction companies commented on stronger client demand in line with the recovery in economic activity and new projects being brought to tender.

Resilient pipelines of new work were highlighted by a steep rise in input buying across the construction sector during February. The latest expansion was the fastest for seven months and commonly reflected pre-purchasing ahead of new project starts. Staffing levels also increased at a sharp pace, extending the sequence of job creation to 13 months.

Around 36% of the survey panel reported longer delivery times among suppliers in February, while only 4% saw an improvement. Delays were overwhelmingly linked to driver and material shortages, as well as international shipping delays. That said, the number of construction firms reporting longer lead times for deliveries was down from a peak of 77% in mid-2021.

Reflective of widespread delivery delays, latest data signalled another rapid rise in input prices, though the rate of inflation eased to an 11-month low. The increase in purchase prices was often attributed to rising raw material and commodity prices amid supply shortages, alongside a lack of transport capacity.

Finally, the near-term outlook for construction activity remained positive in February. Just under half of the survey panel (48%) forecast an increase in output during the year ahead, while only 9% predicted a fall. However, the overall degree of optimism eased to the softest since January 2021 as firms cited concerns about the impact of rising costs and supply shortages.

Usamah Bhatti, Economist at IHS Markit, which compiles the survey said:

“UK construction companies achieved a faster expansion in output volumes in February as the economy recovered from the recent wave of COVID-19 infections related to the Omicron variant. House building had the strongest showing, as signalled by the fastest rise in residential work for eight months.

“Despite continued volatility in price and supply conditions, the overall rate of new order growth accelerated from January to reach the fastest since last August as client confidence improved in line with economic activity as Plan B restrictions were fully lifted.

“Nonetheless, widespread reports of shortages of materials and labour continued to plague the UK construction sector, while rising input costs placed further strain on businesses. It appears that the peak of price pressures has passed as the rate of input cost inflation eased for the sixth month in a row to reach the softest since last March. At the same time, reports of supplier delays were considerably lower than those seen in the middle of last year. Yet, price and supply constraints weighed on overall business confidence, which eased to the softest in just over a year.”

Duncan Brock, Group Director at the Chartered Institute of Procurement & Supply, said:

“The construction sector maintained its growth momentum whilst battling a number of headwinds such as supply issues and higher input costs to put in its best performance for eight months in February.

“All three sectors offered positive news, but housing stormed ahead with the strongest rise in residential building since June last year. The reasons for this improvement ranged from securing contracts in the pipeline of new work and improved deliveries for some materials. That said, hampered supply chains still made business difficult across all sectors and deliveries remained painfully slow.

“Also, the highest rise in order books for six months didn’t do enough to improve future optimism as business expectations dropped to January 2021 levels. Curbing inflation will continue to be a big issue for building firms who will be nervous about securing continuing supply and offsetting price rises to improve business margins, especially if costs continue their skyward trajectory.”

Related news

UK Construction PMI for January 2022

UK Construction PMI for December 2021

UK Construction PMI for November 2021

UK Construction PMI for October 2021

UK Construction PMI for September 2021

UK Construction PMI for August 2021

UK Construction PMI for July 2021

UK Construction PMI for June 2021

UK Construction PMI for May 2021

UK Construction PMI for April 2021