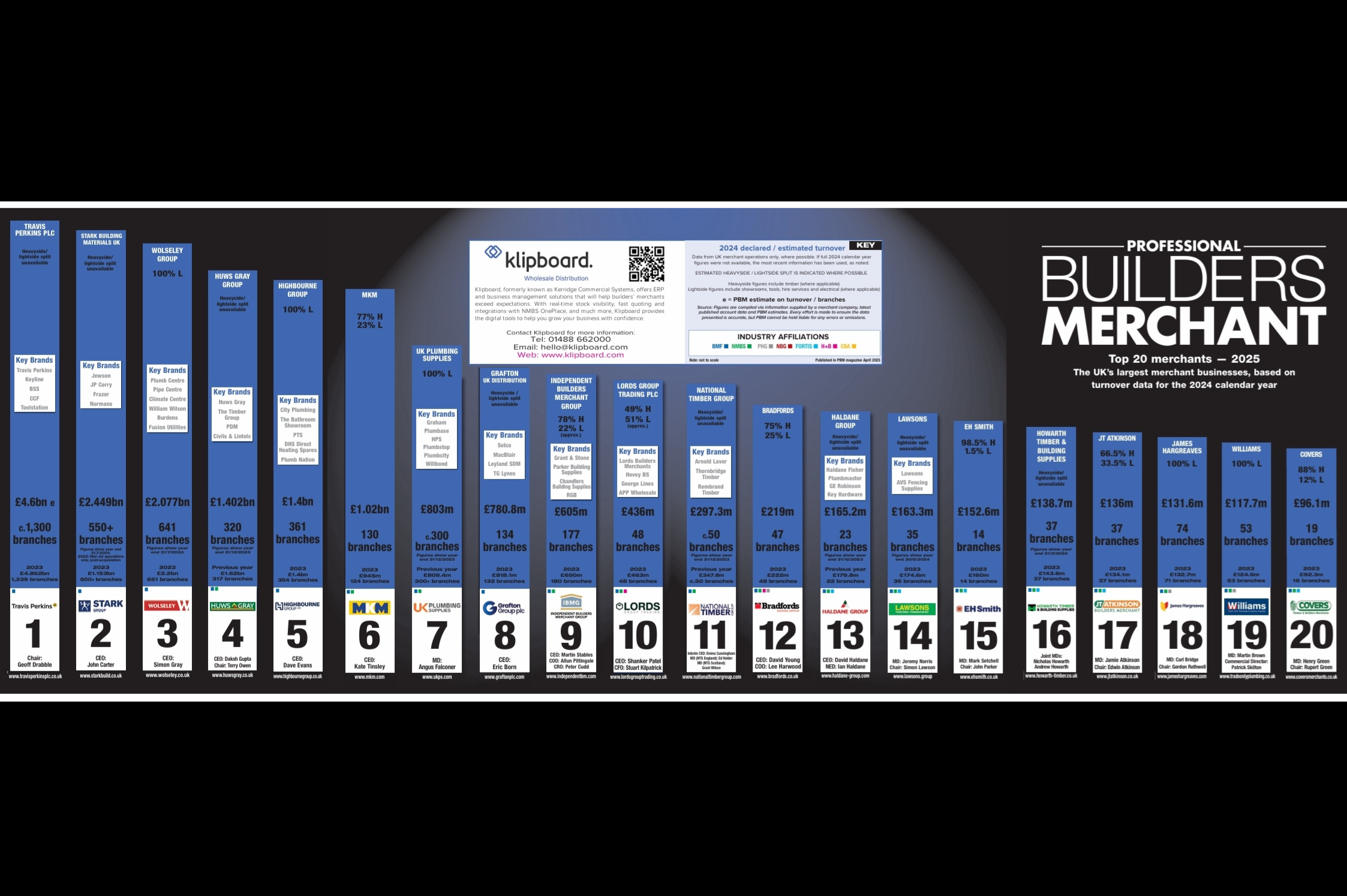

2025 Top 20: As published in our April 2025 edition, PBM goes behind the numbers to consider the performance of the UK merchant sector’s largest businesses during the calendar year of 2024.

Once again, our ‘Top 20’ presents a largely familiar line up with only a couple of positional changes from twelve months previously. Equally, the acquisitional fervour of recent years is even further in the rearview mirror as, outwardly at least, there have been few major developments or fresh organisational changes.

Granted, in the background, one or two of our number have seen additional capital from (new) private equity backers but at the time of going to press, the picture remains generally stable. And as such, the headline numbers hint at the sector’s ongoing challenges with reduced revenues a near universal feature.

However, when considering the responses we’ve received and the details presented in year-end reports, the longer-term view retains an underlying air of optimism as many of our number outline an expectation of an upturn and continue to discuss expansion plans and inward investment.

Looking to our latest countdown itself, Travis Perkins plc remains well clear at the summit although the market leader has been far from immune to the current market challenges…

*** NB: Click here for an enlarged version of the Top 20 graphic ***

1: Travis Perkins plc

2024 turnover = £4.6bn (2023 = £4.862bn)

1,311 branches (1,339 in 2023)

While holding first place, the travails at Travis Perkins plc continue. The business announced a delay to the publication of its financial results due to the Group’s auditor “requesting additional time to complete its standard audit procedures” just a week after it was confirmed that CEO Pete Redfearn was stepping down due to ill health, having only been in post for around six months.

In light with its own reporting practices, the figures include Toolstation UK.

Travis Perkins 2024 Annual Report

2: Stark Building Materials UK

2024 turnover = £2.449bn (2023 = ££1.153bn)

550+ branches (600+ in 2023)

2024 figures show year end to 31.7.24. 2023 figures cover Mar-Jul operations only, post-acquisition.

In contrast, second-placed Stark Building Materials UK was able to report “solid momentum” in the first full year of STARK Group ownership since the acquisition of Jewson et al in March 2023.

A programme of investment, rationalisation and a “strategic shift from centralised leadership to empowering branches with responsibility and accountability” is seen as revitalising a business “that had been underperforming for years,” with a full relaunch of several of its brands, most notably Jewson, alongside the debut of its “Branch of the Future” concept.

Its year end report noted how “active asset management allowed us to invest in bigger, better branches offering a wider product range, always-in-stock guarantee and enhanced distribution through an optimised branch network and reliable delivery services.”

2: Wolseley UK

2024 turnover = £2.077bn (2023 = £2.2bn)

641 branches (651 in 2023)

Figures show year end 31.7.24

Wolseley launched ‘Renewables by Wolseley’ in May 2024 as part of a “long term strategy to enhance the Group’s capabilities in renewable heating and energy efficient solutions.”

Wolseley Group Holdings 2024 Annual Report

4: Huws Gray

Latest recorded turnover = £1.402bn (previous year = £1.62bn)

320 branches (317)

Figures show year end 31.12.23

5: Highbourne Group

2024 turnover = £1.4bn (2023 = £1.4bn)

361 branches (354 in 2023)

Highbourne Group added six new branches in 2024: Doncaster White Rose Way, Doncaster York Road, Herne Bay, Lincoln, Crewe (Showroom) and Basildon. It has already started 2025 with a new City Plumbing outlet in Bristol.

6: MKM Building Supplies

2024 turnover = £1.02bn (2023 = £945m)

130 branches (124 in 2023)

MKM expanded its network last year with sites in Colchester, Cardiff, Shrewsbury, Workington and Rotherham, whilst it acquired Tradeshake and Rab Cordar. More new branches are planned for 2025, with the potential for further acquisitions, as it continues its strategy “to maintain and grow market share” in key geographical areas.

7: UK Plumbing Supplies

Latest recorded turnover = £803m (prior year = £809.4m)

c. 300 branches

Figures show year end 31.12.23

8: Grafton UK Distribution

2024 turnover = £780.8m (2023 = £818.1m)

134 branches (132 in 2023)

Grafton Group plc CEO Eric Born cited the “continuing decline in profitability” in the firm’s UK Distribution arm (Selco, MacBlair, Leyland and TG Lynes) as “RMI demand and consumer confidence remained at historically low levels.”

However, Eric also noted the Group had “continued to upgrade and improve its branch network, open new locations and invest in IT infrastructure to enhance customers’ experience.” He further added: “Whilst uncertainties remain in the short term, we are confident that Grafton is exceptionally well positioned to benefit as conditions improve.” A further share buyback programme has also been announced.

9: Independent Builders Merchant Group (IBMG)

2024 turnover = £605m (2023 = £650m)

177 branches (180 in 2023)

Whilst background speculation on the ownership and control of IBMG continues, the business notes that despite the short-term uncertainty, it “remains focused on profitable sales and market share.” Recent investments into its technology and management information systems in addition to “bringing new capabilities to all of our teams across the business,” meanwhile place it in a “better position than we have ever been as the market recovers in the coming months.”

10: Lords Group Trading

2024 turnover = £436m (2023 = £463m)

48 branches (48 in 2023)

Rounding out the Top 10 is Lords Group Trading which notes the above expectations performance of its Merchanting division, “particularly in the final quarter of FY24 with LFL revenue 11% ahead of Q4 FY23.” In January 2025, a fifth George Lines branch was opened whilst its Plumbing and Heating division demonstrated its commitment to the energy transition with the acquisition of Ultimate Renewables last October.

Looking forward, both organic growth and its M&A strategy focus on opportunities to “broaden the Group’s product range and/or geographic reach in highly fragmented markets.”

11: National Timber Group

Latest recorded turnover = £297.3m (prior year = £347.8m)

c.50 branches

Figures show year end 31.12.23

12: Bradfords Building Supplies

2024 turnover = £219m (2023 = £222m)

47 branches (48 in 2023)

2025 saw the opening of our Barnstaple facility on the 31st March, operating as both a builders’ and P&H merchant.

13: Haldane Group

Latest recorded turnover = £165.2m (prior year = £179.8m)

23 branches (22 in prior year)

Figures show year end 31.12.23

14: Lawsons

2024 turnover = £163.3m (2023 = £174.6m)

35 branches (36 in 2023)

Figures show year end 30.6.24

After a prolonged period of growth, the Group plans to use 2025 to continue to consolidate its customer offering and further integrate recent acquisitions – the Group has made nine acquisitions in the last five years and is 70% bigger than it was prior to the Covid-19 pandemic.

Lawsons has also been investing in websites and has adopted Adobe Commerce (Magento 2) as its Ecommerce platform. The web team have now successfully migrated Lawsons, AVS Fencing, Witham Timber and Oxford Fencing Supplies to the new platform.

15: EH Smith

2024 turnover = £152.6m (2023 = £160m)

14 branches (14 in 2023)

EH Smith is opening a new Kitchen and Bathroom showroom within its busy Solihull branch in Spring. Following the success of EH Smith’s London Design Centre in Clerkenwell, the business is creating a building materials Design Centre in Digbeth, the heart of Birmingham’s regeneration area.

The centre will showcase a wide range of construction materials and incorporate large practical demonstration spaces.

16: Howarth Timber & Building Supplies

2024 turnover = £138,7m (2023 = £143.6m)

37 branches (37 in 2023)

Figures show year end 31.3.24

17: JT Atkinson

2024 turnover = £136m (2023 = £134.1m)

37 branches (37 in 2023)

18: James Hargreaves

2024 turnover = £131.6m (2023 = £132.7m)

74 branches (71 in 2023)

Ongoing plans include the expansion of its delivery fleet, a new warehouse at its head office to increase capacity alongside a solar install at the premises on the road to net zero.

19: Williams Trade Only P&H Supplies

2024 turnover = £117.7m (2023 = £124.5m)

53 branches (53 in 2023)

“Our focus is on continuing to provide best in class service to our loyal trade customers in a market that looks challenging for the foreseeable future. We are also looking to grow our presence in renewables and contract markets.”

2o: Covers Timber & Builders Merchants

2024 turnover = £96.1m (2023 = £92.3m)

19 branches (16 in 2023)

Just missing the threshold are the likes of James Burrell, LBS (which acquired D G Heath, Pontarddulais and Denmans, Caerphilly) and Sydenhams. Sydenhams, for instance continued to invest in the business throughout 2024, completing the acquisition of a merchant site in Shipston-on-Stour in Sept-24 (formerly Shipston Building Supplies) whilst in Oct-24 its brand-new e-commerce website went live, enhancing the offering to customers.

Businesses such as Builder Depot and Markovitz are also on the radar, following their most recently published results.

We are extremely grateful for the support of the sector in compiling this industry barometer.

Industry affiliations / buying group membership:

BMF (20) — All

NMBS (15) — All except TP, STARK Building Materials UK, Wolseley UK, Highbourne Group, Grafton Group

Fortis (6) — Haldane Group, Lawsons, EH Smith, Howarth Timber & Building Supplies, JT Atkinson, Covers

H+B (2) — Lords, Bradfords Building Supplies (exc. plumbing & heating – see below)

PHG (3) — Bradfords, James Hargreaves, Williams

Source: Figures are compiled via forecasted information supplied by each company, latest published account data (as indicated) and PBM estimates. Every effort is made to ensure the data presented is accurate but PBM cannot be held liable for any errors or omissions.

Related news

UK merchant sector Top 20 – 2023 calendar year

UK merchant sector Top 20 – 2022 calendar year

UK merchant sector Top 20 – 2021 calendar year

UK merchant sector Top 20 — 2020 calendar year

UK merchant sector Top 20 – 2019 calendar year

UK merchant sector Top 20 – 2018 calendar year